If you have immigrated recently, it can be a tough task to get a credit or a credit card in a new place. I know it for sure as I changed several countries for the last three years following the expansion of my business — a fintech company and a social lending service provider MicroMoney.

[Note: This is a sponsored article – written by Anton Dzyatkovsky, co-founder of MicroMoney]

Even though in the previous country where you lived you always repaid loans properly and have proved to be an honest credit customer. Even though you used to start your day with a glass of the most expensive champagne and caviar sandwich. It doesn’t mean all your habits and usual sweets of life will be taken into account by the bank system of your new country. Moreover, banks use different credit scoring models and, thus, your credit score varies by a bank or a credit bureau. This information should be considered by both who are going to immigrate and to buy a house or a car on credit and those who need just some money urgently.

So it turns to be a sad story because you become totally dependent on a bank’s scoring system. That also forces you to spend a lot of time chasing down documentation, standing in queues and wrecking your nerves without having any results sometimes. However, I think that my company is able to suggest a solution.

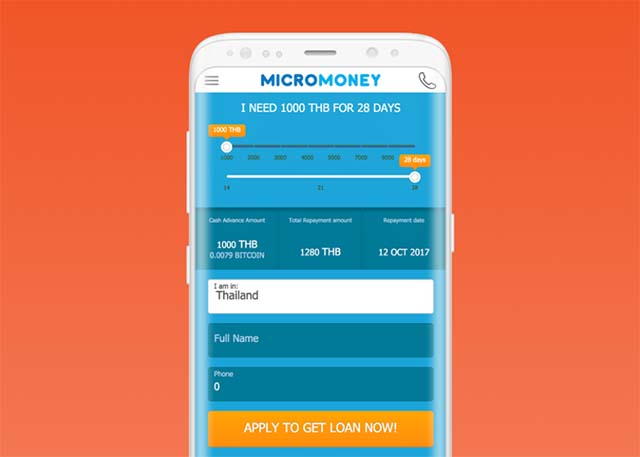

We at MicroMoney need only your smartphone data to provide you a loan. Everything is transparent, so you don’t have to wait for the bank approval or struggle to prove that you are a reliable credit customer. Just download the MicroMoney’s app and it will explore all the data stored on your phone for several minutes and approve (or disapprove) a loan. That seems to be a revolution in the whole bank system as we do it not only very fast but also set a goal is to reduce the cost of loans up to 0% for those users of our ecosystem who follow the rules and return loans on time.

From Credit Score …

Being an immigrant you can hardly get a loan, especially for the first time. To provide a loan, banks check your credit history in a traditional way. To have a credit story you should have had credits or credit cards which actually you don’t have since you are new in this country. It looks like a vicious circle.

As mentioned above, there are hundreds of credit scoring models being used today. The FICO and the Vantage Scores are the most commonly used worldwide credit-scoring models with a scale range of 300-850 to score a borrower. The higher credit score is, the better is your creditworthiness.

Why is it so important for a credit score to be high? The thing is that when you need any loan, the higher credit score you will provide a better bank offer, the lower percentage, the higher chance for your loan application to be approved you will get. And the bigger budget you can apply for, of course.

An immigrant is forced to start a credit history from scratch in a new country. Therefore, it is usually difficult for them to obtain credit cards and mortgages until after they have worked in the new country with a stable income for several years.

However, a good credit score will be reset to zero in the other country even if they are quite close to each other geographically, even if you apply for a loan to a subdivision of the same company that already granted you money before. I know, for example, that Equifax Canada does not share credit information with Equifax in the United States.

… To Mobile Score

Has the world ever been so open, globalized and mobile? Why everything changes but classic banks? Unfortunately, people face this problem all over the world and our company, MicroMoney, can help them.

We consider the loan availability a part of human rights and two years ago started to follow our social mission of financial inclusion for 2 billion of the world’s unbanked. People should have an access to extra money to solve their urgent problems and shouldn’t suffer from the fact that banks of different countries haven’t found a common solution. In 2015, when MicroMoney started to provide social microloans, someone could hardly imagine that scoring of a smartphone would let you get a loan. Today it is the best practice.

Why should you go to the bank now? All the information contains in your smartphone and you don’t have to prove your creditworthiness with a pile of documents anymore. And you also don’t have to be attached forever to the country which appreciates you for your good credit history.

Be free!

Do you think banks’ credit scoring models are too arbitrary when it comes to determining the creditworthiness of new immigrants? Let us know in the comments below.

Images courtesy of MicroMoney, Shutterstock